How is monthly salary income tax calculated in Nepal (FY 2082/83)?

Nepal uses a progressive slab system for salaried employees, set each year in the Finance Act. For FY 2082/83 (Shrawan 2082 – Ashadh 2083), the slabs were defined in Finance Act 2082 — amending the Income Tax Act 2058 — and they differ between single (unmarried) and married (couple) filing status. Below the calculator output, you can see exactly which slab each rupee of your taxable income falls into.

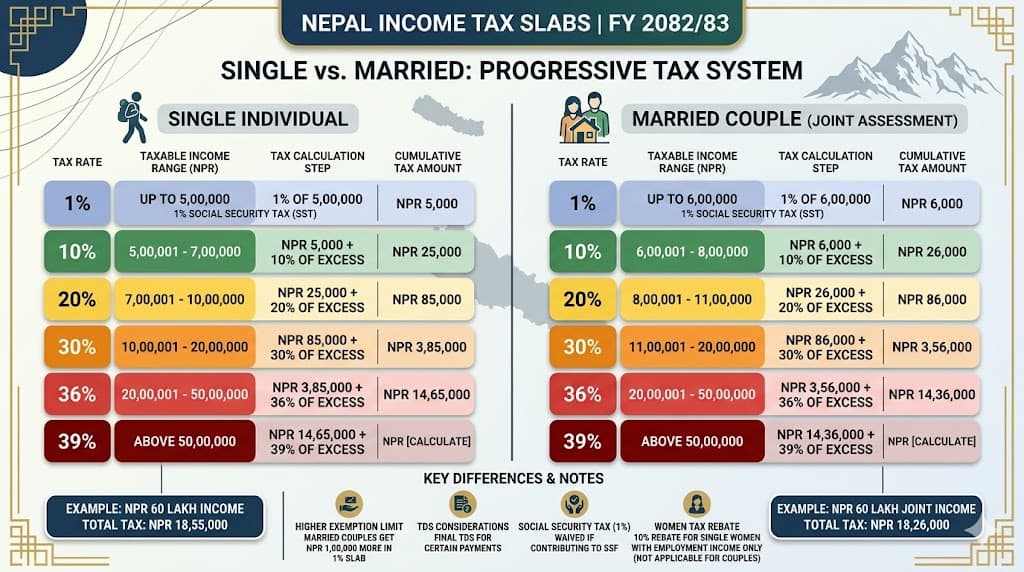

Income tax slabs for FY 2082/83

| Single | Couple | Rate |

|---|---|---|

| First Rs 5,00,000 | First Rs 6,00,000 | 1% (SST) — 0% if SSF participant |

| Rs 5,00,001 – 7,00,000 | Rs 6,00,001 – 8,00,000 | 10% |

| Rs 7,00,001 – 10,00,000 | Rs 8,00,001 – 11,00,000 | 20% |

| Rs 10,00,001 – 20,00,000 | Rs 11,00,001 – 20,00,000 | 30% |

| Rs 20,00,001 – 50,00,000 | Rs 20,00,001 – 50,00,000 | 36% (30% + 20% surcharge) |

| Above Rs 50,00,000 | Above Rs 50,00,000 | 39% (30% + 30% surcharge) — new in FY 2082/83 |

Source: Finance Act 2082 (Income Tax Act 2058 as amended). For section-level detail, see our complete TDS guide.

What changed in FY 2082/83 vs FY 2081/82?

The headline change in Finance Act 2082 is the splitting of the previously flat top slab into two:

- Rs 20,00,001 – Rs 50,00,000 stays at the existing 36% rate (30% base + 20% surcharge).

- Above Rs 50,00,000 attracts a new 39% rate (30% base + 30% surcharge). Previously, all income above Rs 20,00,000 was a flat 36%.

For employees with annual taxable income below Rs 50,00,000, monthly TDS is unchanged between FY 2081/82 and FY 2082/83. The new 39% slab affects only the portion of income above Rs 50 lakh — typically senior executives, partners, and high-earning consultants. Deduction caps (Rs 5,00,000 combined retirement, Rs 40,000 life insurance, Rs 20,000 health insurance) and the 1/3-of-gross retirement ceiling all remain unchanged.

What deductions can a salaried employee claim?

The retirement contributions SSF, PF / EPF, and CIT are added together and capped at the lowest of three values:

- The actual amount you contributed.

- One-third of your gross annual income (the proportional ceiling).

- Rs 5,00,000 per year (the absolute statutory cap).

Whichever is smallest — that is your allowable retirement deduction. Anything contributed above that limit is still saved into your retirement account, but does not reduce your taxable income for the year.

Two other deductions are applied on top of the retirement cap:

- Life insurance premium — deductible up to Rs 40,000 annually.

- Health insurance premium — deductible up to Rs 20,000 annually.

SSF participation also makes the first 1% Social Security Tax slab become 0% — so SSF members save both on the deduction and on the first-slab rate.

Worked example A — statutory cap binds

Gross annual income Rs 20,00,000, with combined CIT + PF + SSF contribution of Rs 7,00,000.

- Actual contribution: Rs 7,00,000

- 1/3 of gross (Rs 20,00,000 ÷ 3): Rs 6,66,667

- Statutory cap: Rs 5,00,000 ← lowest, applies

Allowed deduction is Rs 5,00,000 → taxable income becomes Rs 15,00,000.

- Rs 5,00,000 × 1% = Rs 5,000

- Rs 2,00,000 × 10% = Rs 20,000

- Rs 3,00,000 × 20% = Rs 60,000

- Rs 5,00,000 × 30% = Rs 1,50,000

- Total annual tax = Rs 2,35,000

If the same employee is an SSF participant, the first 1% slab becomes 0% — annual tax drops to Rs 2,30,000.

Worked example B — 1/3-of-gross binds

Gross annual income Rs 13,00,000, with combined CIT + PF + SSF contribution of Rs 6,00,000.

- Actual contribution: Rs 6,00,000

- 1/3 of gross (Rs 13,00,000 ÷ 3): Rs 4,33,333 ← lowest, applies

- Statutory cap: Rs 5,00,000

Allowed deduction is Rs 4,33,333 → taxable income becomes Rs 8,66,667. The remaining Rs 1,66,667 of contribution stays in retirement accounts but doesn't reduce TDS this year.

- Rs 5,00,000 × 1% = Rs 5,000

- Rs 2,00,000 × 10% = Rs 20,000

- Rs 1,66,667 × 20% = Rs 33,333

- Total annual tax ≈ Rs 58,333

Worked example C — high earner with new 39% slab

Gross annual income Rs 60,00,000 for a single filer, with combined CIT + PF + SSF contribution of Rs 5,00,000 (retirement cap binds).

Taxable income = Rs 55,00,000.

- Rs 5,00,000 × 1% = Rs 5,000

- Rs 2,00,000 × 10% = Rs 20,000

- Rs 3,00,000 × 20% = Rs 60,000

- Rs 10,00,000 × 30% = Rs 3,00,000

- Rs 30,00,000 × 36% = Rs 10,80,000

- Rs 5,00,000 × 39% = Rs 1,95,000

- Total annual tax = Rs 16,60,000 (Rs 1,38,333 /month)

Under FY 2081/82 (flat 36% above 20L), the same employee would have paid Rs 16,45,000. The new 39% slab adds Rs 15,000 / year for every Rs 5,00,000 above the Rs 50 lakh threshold.

Calculator vs manual Excel calculation

Most HR teams in Nepal still compute monthly TDS in Excel — copying last year's slab table, manually adjusting for Finance Act 2082 amendments, and patching the formula every time SSF rules or the retirement cap change. Four common mistakes we see in manual spreadsheets:

- Missing the new 39% slab above Rs 50 lakh. Many FY 2081/82 spreadsheets simply extend the 36% rate to infinity. For executives crossing Rs 50,00,000 of taxable income, this under-deducts tax and creates year-end shortfalls.

- Forgetting the 1/3-of-gross retirement ceiling. Excel formulas often hard-code the Rs 5,00,000 cap and miss that for lower-income employees the proportional ceiling binds first.

- Wrong SSF treatment.SSF participants' first slab is 0%, not 1%. Manual calculators frequently overtax SSF members by Rs 5,000–6,000 per year.

- Missing the surcharge in the 36% and 39% brackets. The effective rates are 36% (30% + 20% surcharge) and 39% (30% + 30% surcharge), not flat 30%. Easy to miss in a slab-formula chain.

This online Nepali income tax calculator handles all four correctly, and updates every time the Finance Act changes — so HR teams, salaried employees, and CAs don't have to rebuild their spreadsheet each Shrawan.

Who should use this Nepal income tax calculator?

- Salaried employees in Nepal — verify your monthly TDS deduction is correct before HR finalises payroll

- HR & payroll teams — compute TDS for single and married couple employees with SSF, PF / EPF, CIT contributions in one place

- Chartered Accountants & tax consultants — quick sanity-check during audit or client onboarding, including the new FY 2082/83 39% top slab

- NEPSE investors & freelancers — pair this with our NEPSE CGT calculator and VAT calculator for full-picture tax planning

Nepal Salary Tax FAQ — FY 2082/83

What are the salary tax slabs for FY 2082/83 in Nepal?

For single/unmarried individuals: 1% on the first Rs 5,00,000, 10% on Rs 5–7L, 20% on Rs 7–10L, 30% on Rs 10–20L, 36% on Rs 20–50L (30% + 20% surcharge), and 39% on income above Rs 50,00,000 (30% + 30% surcharge). For married couples filing jointly: 1% on the first Rs 6,00,000, 10% on Rs 6–8L, 20% on Rs 8–11L, 30% on Rs 11–20L, 36% on Rs 20–50L, and 39% above Rs 50,00,000. The 1% Social Security Tax slab becomes 0% for SSF participants.

How is monthly TDS calculated from annual salary in Nepal?

Annual gross income is computed (basic + allowances × 12 + festival bonus). Then deductions are applied: SSF + PF + CIT are summed and capped at the lowest of (a) actual contribution, (b) 1/3 of gross income, or (c) Rs 5,00,000; life insurance is capped separately at Rs 40,000; health insurance at Rs 20,000. The remaining taxable income runs through the FY 2082/83 slab table. Annual tax is divided by 12 to give the monthly TDS that HR deducts.

What is new in FY 2082/83 compared to FY 2081/82?

The biggest change is the new 39% top slab on income above Rs 50,00,000. Under FY 2081/82 everything above Rs 20,00,000 was taxed at a flat 36% (30% + 20% surcharge). Under FY 2082/83 the band from Rs 20,00,001 to Rs 50,00,000 stays at 36%, but income above Rs 50,00,000 now attracts a 39% rate (30% + 30% surcharge). Slabs below Rs 20,00,000 and the deduction caps (Rs 5,00,000 retirement, Rs 40,000 life insurance, Rs 20,000 health insurance) remain unchanged.

What deductions can a salaried employee claim in Nepal?

Retirement contributions (SSF + PF/EPF + CIT) are deductible together — but the combined deduction is capped at the lowest of: the actual amount contributed, one-third of gross annual income, or Rs 5,00,000. On top of the retirement cap, life insurance premiums up to Rs 40,000 and health insurance premiums up to Rs 20,000 are deductible separately. Additional exemptions exist for disabled employees, women in some categories, and remote-area allowances — consult your CA for those edge cases.

How does the combined retirement deduction cap work?

Per Section 63 of the Income Tax Act 2058 (published by the Inland Revenue Department at ird.gov.np), your CIT, PF, and SSF contributions are added together, and the deductible portion is the lowest of three values: (1) the actual combined contribution, (2) one-third of gross annual income, and (3) Rs 5,00,000. Example: on Rs 13,00,000 gross income with Rs 6,00,000 combined retirement contribution, 1/3 of gross is Rs 4,33,333 — lower than both the actual contribution and the Rs 5,00,000 cap — so Rs 4,33,333 is the allowed deduction and taxable income becomes Rs 8,66,667. The remaining Rs 1,66,667 is still saved into your retirement accounts but does not reduce TDS this year.

What's the difference between SSF and PF (Provident Fund)?

SSF (Social Security Fund) is the contributory scheme administered by the Social Security Fund Secretariat (ssf.gov.np) — employees contribute 11% of basic salary, employers contribute 20%, and participating employees are exempt from the 1% Social Security Tax. PF (Provident Fund / EPF) is administered by the Employees Provident Fund — employees and employers each typically contribute 10% of basic salary. Both contributions are deductible from taxable income, but they are separate schemes and have different governing laws. Many private-sector employees contribute to PF; SSF is mandatory for some employer categories.

What is the difference between SST, SSF, and TDS?

SST (Social Security Tax) is the 1% tax on the first slab of taxable income, paid into a national pool. SSF (Social Security Fund) is a separate contributory scheme — employees contribute 11% of basic salary and employers contribute 20%; participating employees are exempt from the 1% SST. TDS (Tax Deducted at Source) is the broader mechanism by which the employer withholds and pays your monthly income tax to the IRD on your behalf.

Is there a tax rebate for women in Nepal?

Yes. Single women with only employment income are entitled to a 10% rebate on the income tax payable. The rebate is not available for married women filing jointly (couple status). This calculator implements the standard slabs and does not auto-apply the women's rebate — apply a 10% reduction to the annual tax output if you qualify, or consult a Chartered Accountant.

Is this calculator official?

No. This calculator implements the standard salaried-employee slabs from Finance Act 2082 and is provided for reference. It does not model edge cases like disability exemption, women's rebate, foreign-source income, or remote-area allowances. Always verify with a practicing Chartered Accountant before filing.